Our platform is designed to cater to the unique needs and interests of Boomers, as well as those who provide services and support to this vibrant demographic.

Our platform is designed to cater to the unique needs and interests of Boomers, as well as those who provide services and support to this vibrant demographic.

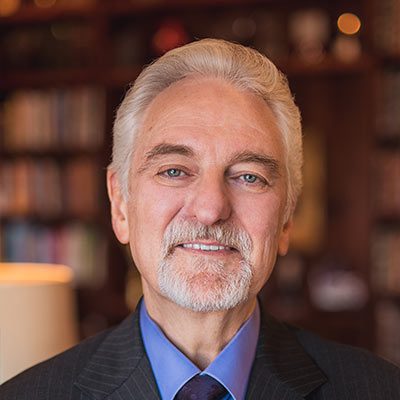

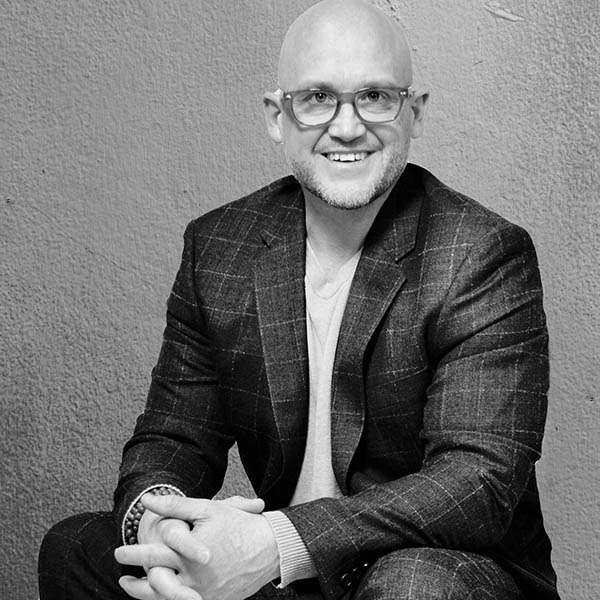

Unlocking Profitable Vacation Rental Investing with Shawn Moore, Founder of Vodyssey.com

Shawn Moore is an active real estate investor, the host of the Vacation Rental Revolution podcast, and the founder of Vodyssey. com, the #1 Vacation Rental Investing Education company in the world.... Read More

.jpg)