Our platform is designed to cater to the unique needs and interests of Boomers, as well as those who provide services and support to this vibrant demographic.

Our platform is designed to cater to the unique needs and interests of Boomers, as well as those who provide services and support to this vibrant demographic.

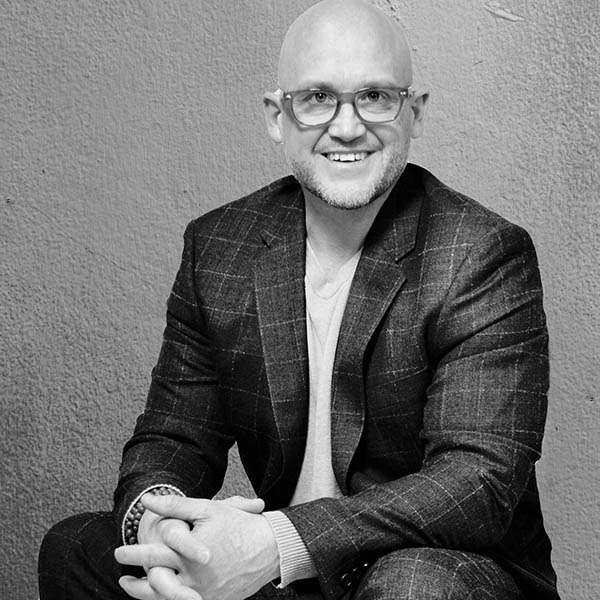

How to Achieve Financial Freedom in the Dentistry Market with Dr. Tony Feck

Episode #379: In today's episode of the "Let's Go Win" podcast, I sit down with Tony Feck, founder of Sunrise Dental Solutions, to dive deep into the financial aspects of running a dental... Read More

.jpg)